Once again in December 2009 CONTROL magazine published its list of TOP-50 Automation & Control suppliers – with separate rankings for global and N. America.

Since these are all public companies, the data is about a year old – for their fiscal years 2008. There seems to be no real solution to this ‘old data’ problem. 2009 will tell a different story.

At $87,7B the top-50 grew about 16% in 2008, compared with 17% in 2007. Growth for North America was 4,6% to $22.9B compared with 5% in 2007.

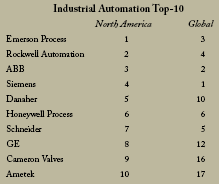

Globally, there was no significant change among the leaders and the top six are now: Siemens, ABB, Emerson, Rockwell, Schneider and Honeywell.

There was no change in the top-three suppliers in the N. American market. Once again, Emerson was #1 on the list with revenues of $3,4B, up 9,6%, and extending market share slightly from 14% to 15%. In second place, Rockwell grew at nearly 11% to $2,9B with market share at 12,5%. In third place was ABB, with revenue of about $2B and minimal growth (3%), with 8,5% market-share. Clearly ABB has shifted to global focus.

In fourth place for N. America was global leader Siemens, with about 3,5% growth to $1,4B. If Siemens wants to grow they will need to make an acquisition. Cannot be Rockwell (anti-trust blockage) but perhaps Honeywell (which slipped to No. six (behind Danaher), or Invensys which fell out of the top-10 (now #14) with 10% lower revenues, behind Endress & Hauser which grew 8,5% to $1,8B.

GE and Fanuc had not broken up yet in 2008, but they were ranked separately, Fanuc is No. 11 and GE No. 12, both at about $1,8B.

Globally, Siemens is still 1,5 times bigger than its nearest rival, ABB, which in turn is more than twice as big as any of the next – Mitsubishi, Emerson and Schneider, all about equal. Japanese Yokogawa is apparently faltering.

The only strategy which would enable the top few to get higher on the rankings is through merger or acquisition. 2010 will be the year of fallout.

Here are a few of my favorite mid-size companies, all growing steadily in the rankings to approach the next tier:

* National Instruments #23 at $800M.

* Phoenix Contact #15 at $1735M – more than double its competitor Weidmuller which is #24 on the list.

* Beckhoff is #41 at $406M and #49 in N. America at $40M.

* OSIsoft got just an honourable mention on the global list, but was #35 at $90M on the N. American ranking.

* Mini-conglomerates (bag of smaller, acquired companies) – Ametek ($1,4B #17); Spectris ($1,2B #19); Roper ($680M #28).

Freemium – a plan for ISA resurgence

ISA membership has been declining steadily in recent years. Today, there are about 28 500 members, including reduced-dues and non-paying lifetime members and students. The surprise is that USA membership has declined to only about 16 000.

With a plethora of high-content information sources available in the Internet ‘free’ paradigm, paying $100 per year for ISA membership is an anachronism. The dues are simply not matched by the value that ISA purports to provide.

A bridge to the future is possible – offering ‘freemium’ membership for anyone interested in automation, anywhere in the world. These could be non-voting members, with the offer of upgrade to full membership upon payment of regular dues. Look up the word freemium in Wikipedia.

There are many way to structure free membership while optimising value. Freemium members would not be members of an ISA section and would not have any voting rights. But they would be able to contribute content to ISA magazines and blogs, and receive discounts for training and attendance at ISA conferences. This would ‘cost’ ISA very little, and yield significant benefits. It will lead to a much higher level of engagement and greater revenue opportunities.

Regular paid membership will increase significantly as freemium members transfer to full membership through clear value offerings. The regular dialog and conversion results will provide feedback on the value of membership and allow development of new member offerings.

As more and more people recognise the value of ISA membership, the conversion rates (from free to reduced-dues and then full membership) will climb to an estimated 25 000 to 75 000 new members. This approaches the number I previously promoted as a goal and still think is a viable objective.

Jim Pinto is an industry analyst and commentator, writer, technology futurist and angel investor. His popular e-mail newsletter, JimPinto.com eNews, is widely read (with direct circulation of about 7000 and web-readership of two to three times that number). His areas of interest are technology futures, marketing and business strategies for a fast-changing environment, and industrial automation with a slant towards technology trends.

© Technews Publishing (Pty) Ltd | All Rights Reserved

printer friendly version

printer friendly version